In the ACA, Texas chose Gold. The data explains why.

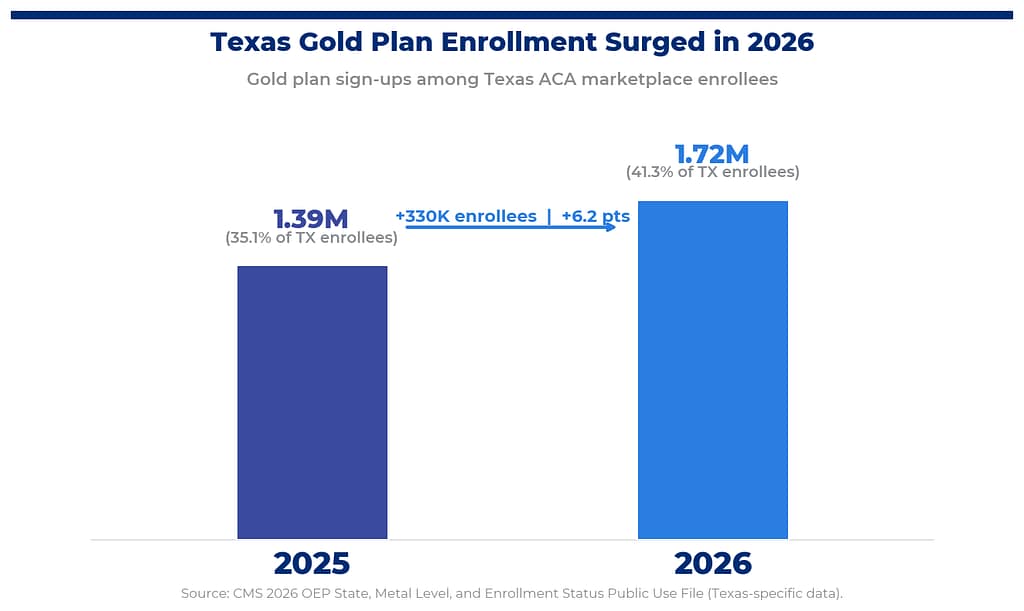

Gold Plans Led Texas Enrollment in 2026

Against a backdrop of national ACA enrollment declining nearly 8%, Texas added more than 200,000 plan selections in 2026. That 5.2% increase represented the largest numerical gain in the country.

That growth is notable, but the data showing the composition of that growth is the more significant story.

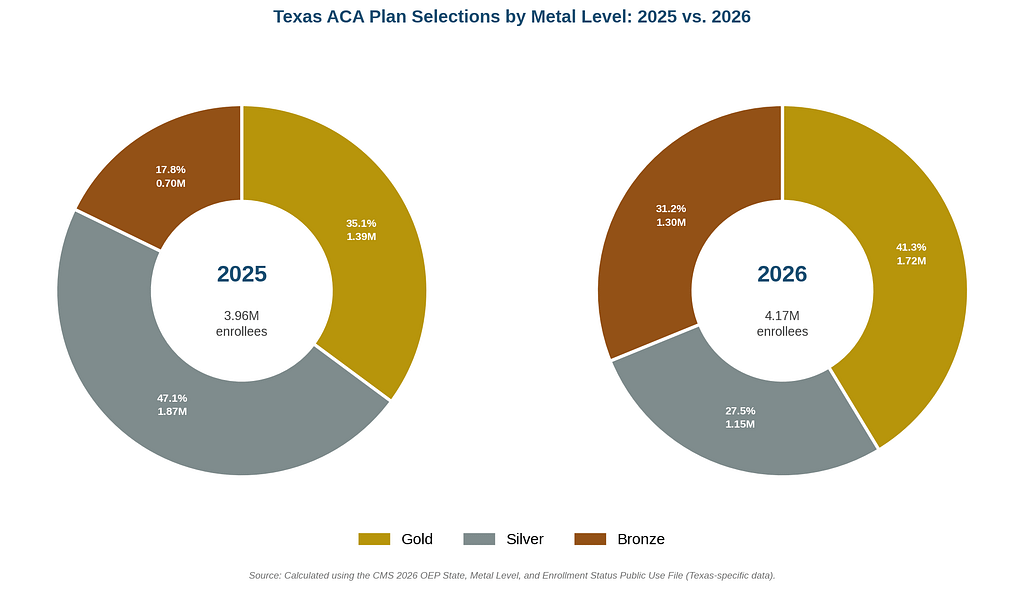

Bronze enrollment was the expected outcome as enhanced premium tax credits expired and consumers faced real cost decisions for the first time in four years. Instead, Gold plans became the single most common plan type in Texas. More than 1.7 million Texans selected Gold coverage in 2026, making it the most chosen plan tier in the state at 41.3%.

That outcome is not accidental. It is the result of a state that optimized its market structure in advance of exactly the conditions that arrived in 2026. This is the story of Senate Bill 1296, a bipartisan Affordable Care Act bill passed unanimously in 2021, that has made better plans more affordable in Texas than in many other states.

The Gold Plan Surge: What It Means for Texas Consumers

The Gold Plan Surge: What It Means for Texas Consumers

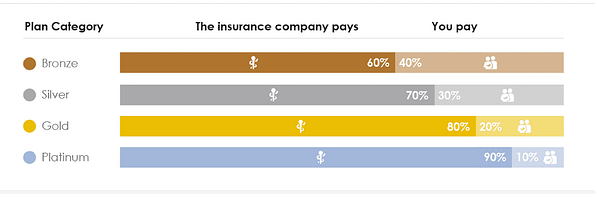

The metal-level distinction is not a mere labeling difference. It reflects the level of financial protection a plan provides, measured by a term known as actuarial value (AV), the share of covered medical costs the insurers pay on average. Bronze plans cover 60%; Silver covers 70% — sort of; Gold covers 80%; and Platinum covers 90%.

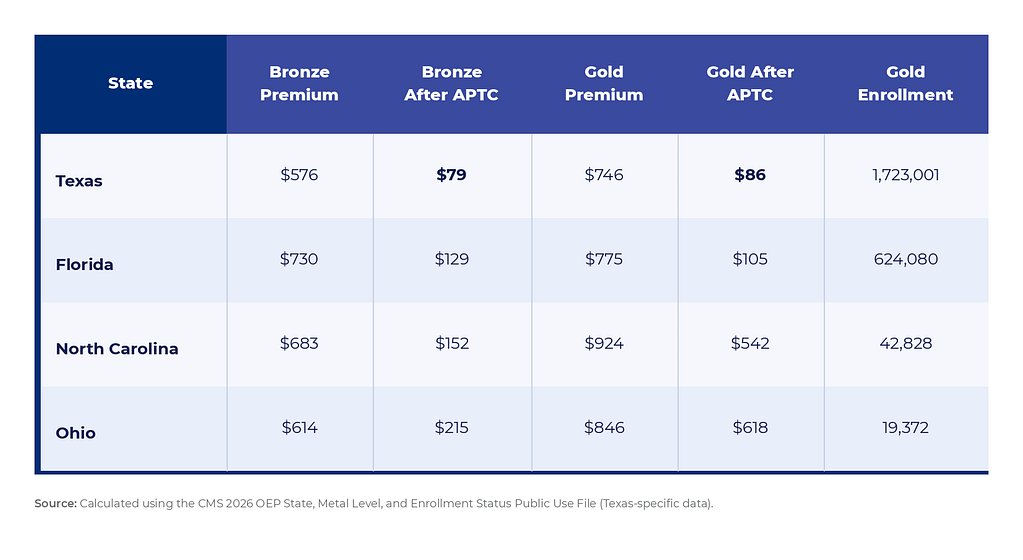

When Texans selected Gold plans in 2026, they were paying only $7 ($86 versus $79) more per month than Bronze after subsidies, but getting meaningfully stronger financial protection in return. Gold’s 80% AV covers more of the covered medical costs than Bronze’s 60%. That price-value relationship is what drove 1.7 million Texans toward Gold, and it is a better coverage than a Bronze-dominant market would have procured. In states without Texas’ market structure, Bronze was the dominant outcome. In Texas, Gold was.

Certain low-income enrollees (those making less than 250% of the Federal Poverty Level) who choose silver-level plans are eligible for extra benefits, known as cost-sharing reductions (CSRs). These CSRs increase the effective actuarial value of Silver plans to 94% for enrollees making less than 150-200% FPL, and to 87% for those making between 150-200% FPL, and to 73% for those at 200-250% FPL, according to the Kaiser Family Foundation.

How Gold Beats Silver on the Marketplace

That CSR structure matters most for the income profile of Texas’ marketplace population. In 2025, 3.1 million Texas, or 75% of total enrollment, had incomes at or below 200% of the Federal Poverty Level (roughly $30,000 for an individual or $60,000 for a family of four). For this population, CSR-enhanced Silver plans can carry actuarial values between 73% and 94%, more protective than Gold on paper.

But as Silver after-APTC premiums nearly tripled in 2026, those enhanced plans became significantly less accessible for many of the families they were designed to serve. For a large portion of Texas’ marketplace population, Gold became the best available option, either the strongest coverage at the lowest price for those above the CSR threshold, or the most accessible meaningful protection for lower-income families priced out of Silver.

While the data does not track where individual Silver enrollees went, the directional shift is clear. As Silver enrollment fell, Gold and Bronze both grew. For those who moved into Gold, the transition represents a plan with strong financial protection at a net premium that Texas’ market structure helped keep within reach. For those who moved into Bronze, the coverage is less protective, but still provides real and meaningful benefits to those covered by it, including $0 out-of-pocket preventive care.

The reason Texans had access to affordable Gold plans — when enrollees in most other states did not — comes down to SB 1296, which kept Gold plan net premiums competitive as the broader subsidy environment tightened. Benefit generosity declined in 2026, but Texas’ deliberate market structure meant that decline landed at Gold rather than Bronze. Not many other states can say that, a distinction that matters for 1.7 million Texans.

While Sticker Prices Rose, Net Premium for Gold and Bronze Held

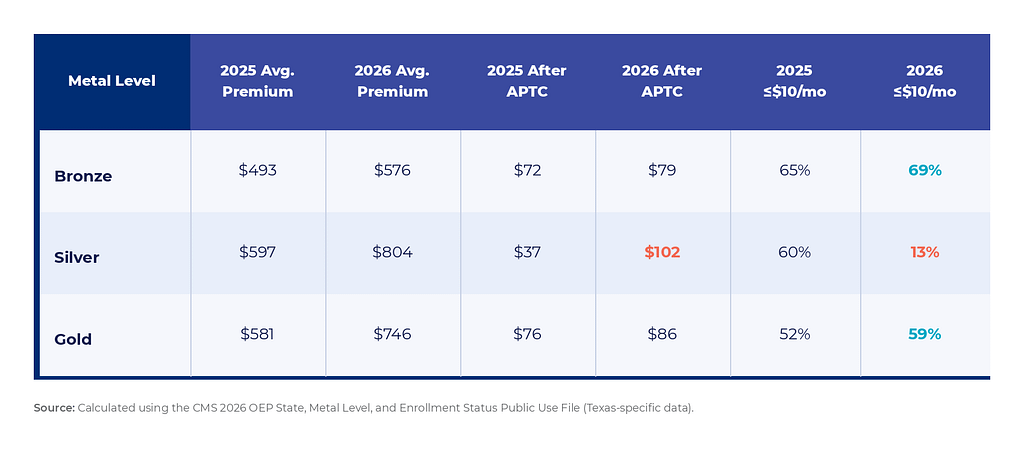

Sticker prices rose across all metal levels in Texas between 2025 and 2026. Bronze premiums increased 16.8%, from $493 to $576. Gold premiums rose 28.4%, from $581 to $746. Silver premiums saw the largest increase, rising 34.7%, from $597 to $804, though this is largely structural. Under Texas’ SB 1296 premium alignment framework, a higher Silver Benchmark premium generates larger tax credits across all metal levels, which is why gross premium growth does not directly translate into higher costs for most enrollees.

For the roughly 95% of Texas consumers who received Advanced Premium Tax Credits (APTC), those sticker price increases largely did not reach them. More than half (59%) of Texas’ 1.7 million Gold enrollees paid $10 or less per month in 2026, up from 52% in 2025. Bronze saw the same pattern rising from 65% to 69%. For consumers who engaged with the market, Gold landed at $86 per month after subsidies and Bronze at $79. Net premiums were stable for most Texans despite the headline increases.

The story looks different for those who did not shop. Active re-enrollees averaged $79 per month less in after-APTC premiums than auto-enrollees, a gap we examine in a related piece.

Texas vs. Peer States After-Subsidy Affordability

The data suggests Texas consumers fared better on after-subsidy costs than most other states in HC.gov. The weighted average after-APTC premium across Bronze, Silver, and Gold plans in Texas was $88, compared to a national average of $136. Among large-enrollment states, Florida ($104) is the closest comparison.

The gap points to Texas’ premium alignment framework as a meaningful factor as more Texans were able to find affordable Gold plans than residents in most other states, a pattern that held even as enhanced subsidies expired.

What the 2026 Data Confirms

In 2026, Texas demonstrated that state-level policy decisions can meaningfully shape outcomes when market conditions shift. Against a national backdrop of declining enrollment and a predicted Bronze surge, Texas grew its total enrollment, made Gold the most selected plan in the state, and kept net premiums low enough that more than half of Gold enrollees paid less than $10 a month. That is the direct result of SB 1296, a structure that, while built before the crisis arrived, worked exactly as intended when it did.