When examining the 2026 ACA enrollment data, a clear line emerged between two groups of consumers: those who actively chose a plan during open enrollment, and those who were automatically renewed into their prior year coverage plan without taking any action. The difference in outcomes between those two groups is one of the most revealing findings in this year’s data.

Texas’ 4.17 million plan selections are divided into three enrollment types: active re-enrollees (2,072,012) who returned to the marketplace to choose a plan; auto re-enrollees (1,335,905) who were passively renewed; and 764,316 new consumers who were not enrolled in Marketplace coverage at the end of 2025.

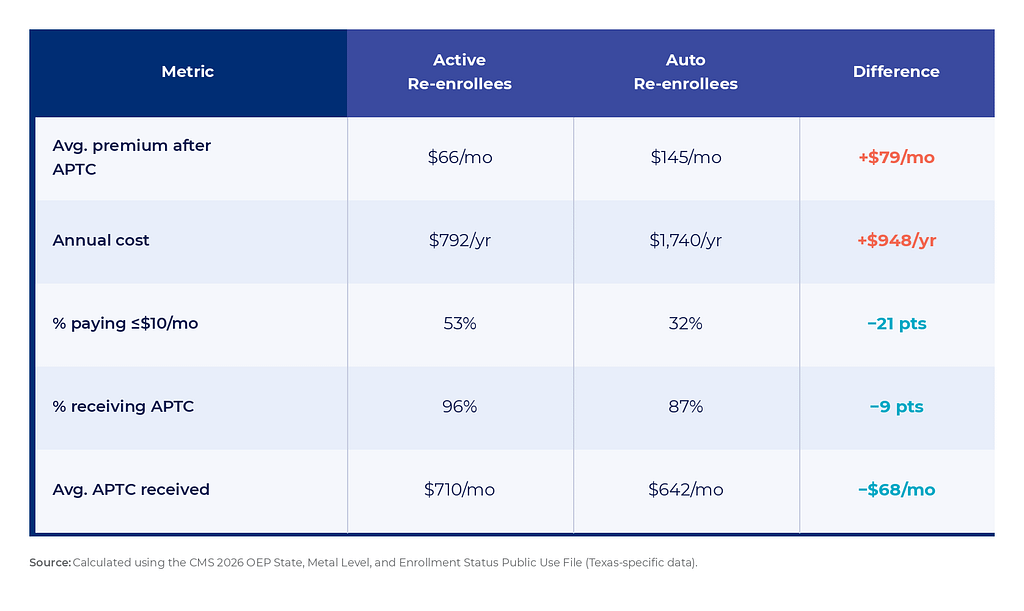

Passive Re-Enrollees Will Pay Nearly $1,000 Per Year More Than Active Re-Enrollees

The premium gap between active and passive enrollment is notable. Active re-enrollees averaged $66 per month in premiums after subsidies. Passive re-enrollees paid more than twice as much at $145 per month. This $79 monthly difference, totaling $948 per year, represents the measurable cost of not shopping.

Differences in income do not explain the gap. Both groups are heavily concentrated at lower income levels. The divergence reflects plan selection: active re-enrollees made deliberate choices in a changed market, while auto re-enrollees remained in prior-year plans that, in many cases, no longer represented the best value.

It is also worth noting that only 87% of auto re-enrollees received premium tax credits, compared to 96% of active re-enrollees. That 9% point gap suggests a share of auto re-enrollees are paying full or near-full premiums.

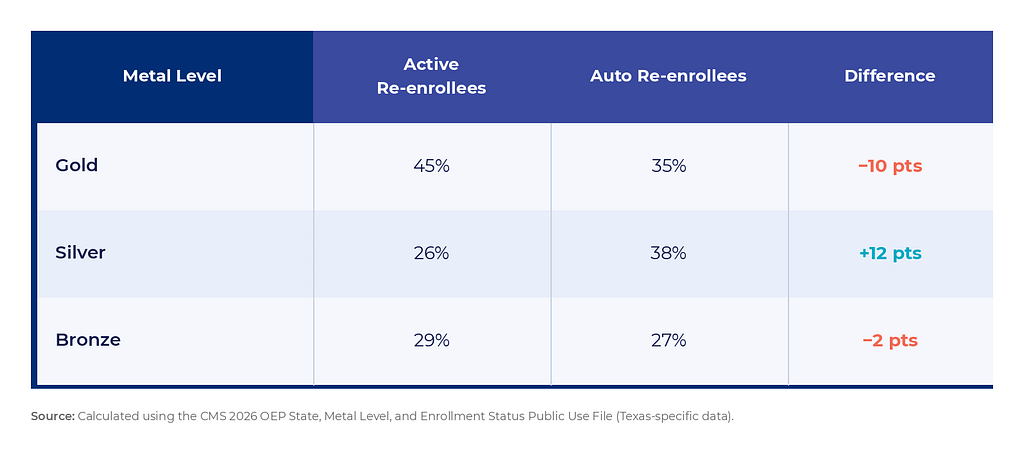

Active Shoppers Found Better Coverage, Not Just Lower Premiums

The premium gap tells part of the story. The plan selection data tells the rest.

Among active re-enrollees, 45% chose Gold plans, 29% chose Bronze, and 26% chose Silver. Among auto re-enrollees, 35% remained on Gold, 27% on Bronze, and 38% on Silver. The auto re-enrollee Silver share was nearly 50% higher than the Silver share among active selectors. Active shoppers did not simply find cheaper plans, they disproportionately landed in the plan tier with the lowest out-of-pocket cost exposure.

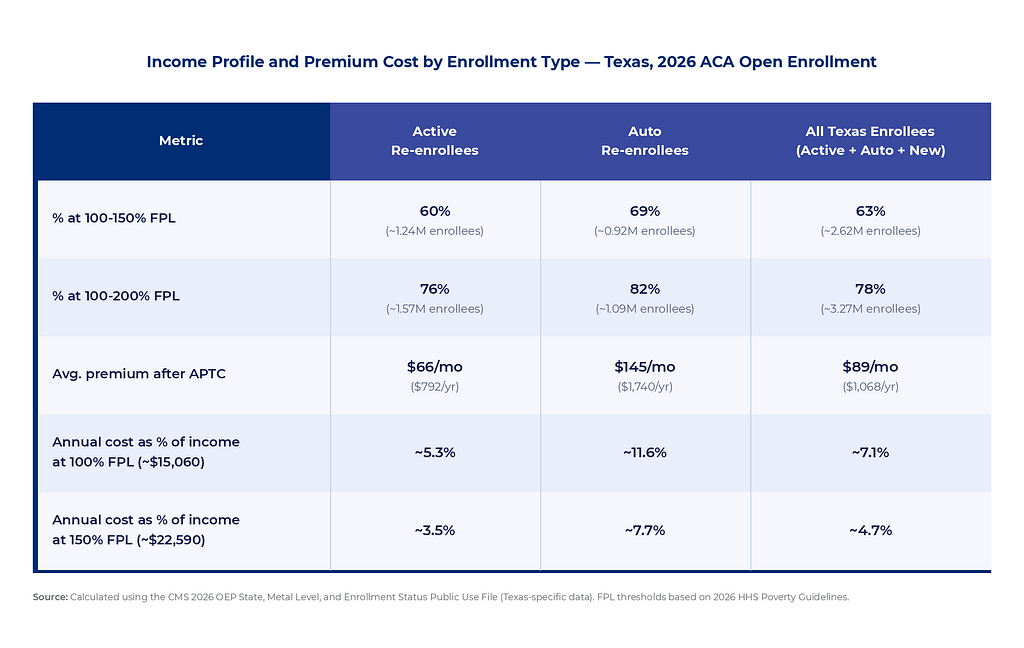

Who the Auto Re-enrollees Are

Auto re-enrollees are not a higher income group indifferent to premium costs. 69% of auto re-enrollees have incomes between 100-150% of the Federal Poverty Level — roughly $18,000 to $27,000 per year for an individual, or $38,000 to $55,000 for a family of four. At those income levels, $145 per month represents a meaningful share of household income. The data does not explain why, but it is clear that in 2025, engaging with the market produced better outcomes. The opportunity was there for those who acted on it.

The affordability floor that Texas’ market structure provides, and maintained in part through the premium alignment mechanism established by Senate Bill 1296, was available to these consumers. Active re-enrollees and new consumers at the same income levels accessed it. Auto re-enrollees largely did not.

What the Data Points To

The 2026 data does not identify why auto re-enrollees did not shop. It records only that they did not, and what that cost them. What it does suggest is that the gap between active and passive outcomes is large enough to warrant attention. The case for exploring ways to increase awareness is evident. What is less established is which awareness-raising mechanisms are most effective. That is the question the state should be asking.

Because the state pays none of the premium dollars in the marketplace, investments in outreach and awareness are worth examining through a cost-efficiency lens. It is possible that targeted, measurable investments in awareness could reduce burden on other state programs such as Medicaid, Directed Payment Programs, and local indigent care funding, though that case warrants further study. For a consumer, the difference between shopping and not shopping in 2026 was nearly $1,000 per year and a meaningful difference in coverage quality. This is the scale of impact that better awareness could deliver.

In future open enrollment periods, the message should largely center around enrollees going to the marketplace and shopping for a plan that works for them and their family. This typified the kind of message we encouraged at Texas 2036. It is clear that the marketplace worked for Texans who engaged with it.