Nearly 5 million Texans are uninsured, which limits almost one out of every five Texans from being able to access affordable care. These numbers contribute to Texas ranking among the worst states for many preventable health outcomes such as maternal mortality and diabetes — and makes it harder for businesses to find the healthy workforce our economy needs to thrive in the future.

As Texas continues to grow, adding nearly 10 million people from 2020 to 2036, it’s critical we adopt policies that will lower the number of uninsured so all Texans have the opportunity to access affordable care.

Why does the number of uninsured Texans matter?

Health care in Texas is broken. For many, insurance is unaffordable – to the point of being unobtainable. For others, even those with insurance, the costs of premiums and care are unsustainable. Average annual premiums to cover a family on employer plans (the most common way insured Texans are covered) are over $20,000 – that’s one-third of the average Texas household’s total annual income. And for other Texans, the price of care and available of insurance coverage aren’t the only barriers; rather, a lack of hospitals, doctors, and access to care prevents many Texans from receiving the care they need when they need it. The size and scope of these problems can be overwhelming, and each problem needs to be addressed. But one problem, in particular, stands out when comparing Texas to the nation’s 49 other states: Texas has the largest uninsured population – by far – and the highest uninsured rate – by far.

Five million Texans lack insurance – nearly one in five Texans – which limits their ability to access affordable preventative care and often forces costs to be absorbed by the public via safety net programs. For many of these Texans, policy choices made at the state and federal levels have left them with no realistic path to coverage. Consider the following hypothetical examples of full-time workers in essential jobs:

- A 24-year-old grocery clerk in Houston with one child making $16,000 a year – slightly above minimum wage for a full-time job. On the individual market, insurance would cost $3,671 per year for an Affordable Care Act Silver plan, or 23% of annual income. And out of pocket costs could total $8,550 before insurance helped pay any bills.

- A 42-year-old housekeeper in San Antonio with two children making $20,000 a year — about $10 an hour for a full-time job. On the individual market, insurance would cost $4,909 per year for an Affordable Care Act Silver plan, or 20% of annual income. And out of pocket costs could total $8,550 before insurance helped pay any bills.

- A married 50-year-old couple in Dallas with three children, who were laid off and now stringing together gig labor as delivery drivers making $30,000 a year combined. On the individual market, insurance would cost $13,987 per year for an Affordable Care Act Silver plan for them both, or 47% of annual income. And out of pocket costs could total $17,100 before insurance helped pay any bills. Combined, that’s more than their annual income.

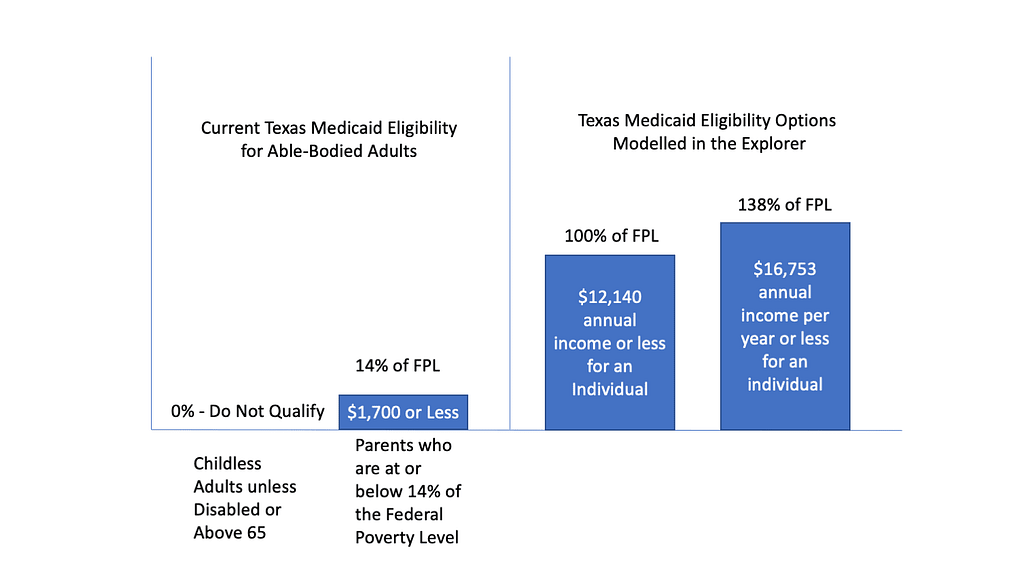

Because of policy choices made by the Texas government, individuals like these have no path to affordable insurance: they would not have access to either Medicaid or individual market subsidies. For these Texans – several of the hundreds of thousands falling into this “coverage gap” — our state policy choices have eliminated their realistic choices and our state government has the power to give these Texans choices. While these Texans are most in need of help, all Texans could benefit from more affordable coverage options.

Developing affordable health insurance solutions for the growing number of uninsured is critical so that families and individuals can:

- Access the medical care they need and not skip or postpone medical treatment because of costs. Three out of every four Texans without health insurance report skipping care because of costs.

- Reduce the threat of significant medical debt from accessing emergency care. According to a 2018 survey published by the Financial Industry Regulatory Authority, or FINRA, Texas has 6.2 million adults with unpaid medical bills, or 29.0% of the population.

Who are among the almost 5 million Texans who are uninsured?

More than 80 percent of uninsured Texans are working-age adults. Over 850,000 – 17 percent – are children. Many uninsured are middle class: nearly half (45%) of uninsured Texans could be considered moderate to middle-income, earning at least twice the ; for a family of four, that would be more than $50,000 per year.

Note: The federal poverty level for a family of four in 2018 is $25,100. Source: U.S. Department of Health and Human Services, ASPE 2018 Poverty Guidelines.

The Explorer focuses on options to increase the number of non-elderly adults with insurance for several reasons:

- Non-elderly adults comprise the overwhelming majority of the uninsured population;

- There is a substantial gap in existing good health coverage options for the non-elderly adult population;

- The second largest group – children – already have options available to them, such as CHIP; and

- Studies show that children with parents who are insured are more likely to be insured themselves. Solving for adults will have positive spillover impacts on the uninsured child population.

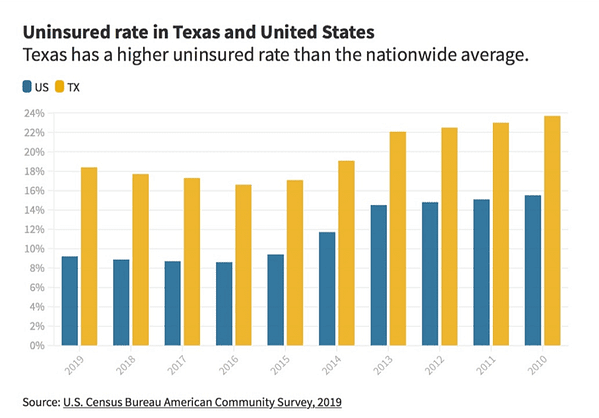

In 2018, the percentage of uninsured in Texas was 18%, which was the highest in the country and much higher than the closest states, Georgia and Oklahoma (14%). That said, Texas’ uninsured rate varies throughout the state.

What Health Coverage Policy Options Are Available to Texas Legislators Today?

In the 87th Legislative Session, Texas legislators have a multitude of policy combination scenarios for helping to connect more Texans with health insurance. Texas 2036’s Health Coverage Policy Explorer analyzes more than 500 discrete scenarios, categorizing policy options by the two primary federal funding sources available today:

- Options related to expanding or improving the Texas Medicaid program.

- Options related to private insurance plans on the Individual Marketplace under the Affordable Care Act.

The Health Coverage Policy Explorer allows all Texans to explore alternatives from each of these sets and combine different options to find ways of maximizing federal funding streams and covering more Texans.

Health Coverage Policy Options

| Combine options from different sets, or only explore one |

| Set 1. Medicaid Expansion |

*Choose no more than one option from Sets 1 and 2 |

| Full Expansion to 138% of |

|

| Partial Expansion to 100% of FPL (Federal 1115 Waiver) |

|

| Targeted Population Expansion (Federal 1115 Waiver) |

|

| Set 2. Medicaid Program Improvements |

|

| Modified Expansion: Indiana Plan (Federal 1115 Waiver) Coming Soon |

|

| Set 3. ACA Marketplace – State improvements |

*No choice restrictions |

| Focused Rate Review |

|

| State-Based Exchange |

|

| Set 4. ACA Marketplace – Federal 1332 Waivers |

*Choose no more than one from this set |

| Reinsurance Pool: Conditions-Based |

|

| Reinsurance Pool: Claims-Based |

|

|

Subsidy Optimization |

Note: FPL stands for federal poverty level, used to determine Medicaid and ACA Subsidy eligibility. Source: U.S. Department of Health and Human Services, ASPE Poverty Guidelines.

1. Medicaid Policy Options – Expansion and Improvements

At the end of 2020, Texas Medicaid provided health insurance to 4.4 million Texans. Currently, it’s available to adults with low incomes in specific vulnerable populations, including:

- Pregnant women;

- People who are blind, who have a disability, or who have a 65 or older family member with a disability in the household; and

- Very low-income parents and people responsible for a child who is 18 or younger.

To reduce the number of uninsured people, Texas 2036’s Health Policy Coverage Explorer models three policy options that change Texas’ Medicaid eligibility to cover more Texans. Soon we will also model a policy proposal to improve Medicaid by incorporating additional personal responsibility components, such as small premiums, co-pays, and incentives for healthy behavior choices like smoking cessation, which are inspired by Indiana’s program.

2. Individual Marketplace under the Affordable Care Act

In 2020, more than 1.28 million Texans shopped for health insurance plans in the Affordable Care Act insurance marketplace, which is run by the federal government at HealthCare.gov. Federal subsidies are available to those Texans who participate, based on citizenship, age, and income.

Texas 2036’s Health Coverage Policy Explorer analyzes two different sets of insurance marketplace policy options to reduce the number of uninsured in Texas:

- Affordable Care Act Improvements (Or Texas’ Individual Marketplace Improvements).

- The Health Coverage Policy Explorer models the impacts of Texas implementing a State-Based Health Insurance Exchange and/or a Focused Rate Review process to improve the insurance marketplace. More than a dozen states, including Virginia and Pennsylvania, have decided it would be better for their citizens to run their own State-Based ACA Marketplace, instead of relying on the Federal Government to do so. The Health Coverage Policy Explorer models the policy options Texas can adopt to improve the marketplace for Texans, such as running the ACA Marketplace at a lower cost.This option would also allow the state to collect more than $200 million in insurance fees that Texans are sending to the federal government to operate the ACA Marketplace today.

- The Explorer also models the impact of a Texas Focused Rate Review, which would increase gross premiums of the “benchmark plans” offered in the ACA Marketplace to reflect actual program costs. The premiums of the benchmark plans are used to calculate the total subsidies for which individuals are eligible. Higher benchmark premiums mean more federal subsidies. Those Texans who are eligible for subsidies will continue be able to purchase benchmark plans for the same amount they do today, because the increased federal subsidies will cover the increased benchmark premium costs. The important advantage is that they will also find non-benchmark plans at lower net premiums because the non-benchmark gross premiums won’t be impacted by Focused Rate Review, and because federal subsidies are set from the (now) higher benchmark premium rate. Increased federal subsidies will allow Texas to maximize every federal dollar available and provide individuals the opportunity to purchase the insurance plan that is right for them and their families.

- Federal 1332 Waivers (Or Innovation Waivers). Texas can pursue federal waivers to add a range of innovations to the health insurance marketplace. These waivers are negotiated extensively with the federal government. It remains to be seen what approach the new presidential administration will take with regards to 1332 Waivers. The Health Coverage Policy Explorer models options for:

- Reinsurance Pools (both claims-based and condition-based), which fund high-cost claims or individuals outside of the marketplace to reduce average premiums; and

- Subsidy Optimization, which is a new concept to improve how subsidies are allocated and optimized to increase their effectiveness. This option requires that Texas first establish a state-based insurance exchange (see ACA Improvements above).

What results does the Health Coverage Policy Explorer Show?

Below are some health coverage policy options and combinations that have been discussed by Texas legislators for lowering the number of uninsured Texans. These demonstrate the range of possibilities available to lawmakers and effects over the next four years.

Within the Health Coverage Policy Explorer, Texans can review the default assumptions and set their own for factors such as the percentage of eligible Texans expected to participate in coverage. However, the numbers listed below show the default assumptions our experts utilized.

Income, citizenship and residency status of the uninsured Texan determine the availability of coverage. We have broken down Texas’ non-elderly adult uninsured population into six categories and indicated the possible policies that may benefit them. The fiscal impact (in terms of state budget outlays) and benefits (in terms of the increased number of insured Texans) will depend on the type and combination of policies selected.

Uninsured Texans Aged 19-64, by Income Level, and Various Health Coverage Policies That Could Aid Them)

| Percentage of |

Group of Adults, Ages 19-64 |

Population |

Full Medicaid Expansion |

Partial Medicaid Expansion |

Targeted Medicaid Expansion |

Focused Rate Review |

Subsidy Optimization |

Reinsurance Pools |

Medicaid Improvments (Coming Soon) |

| 0-100% |

Citizens & Eligible LPRs |

797,097 |

✔ |

✔ |

✔ |

✔ |

✔ |

|

✔ |

| 101-138% |

Citizens & Eligible LPRs |

356,986 |

✔ |

|

✔ |

✔ |

✔ |

|

✔ |

| 0-138% |

Medicaid Ineligible LPRs |

69,681 |

|

|

|

✔ |

✔ |

|

|

| 139-400% |

Citizens and LPRs |

1,656,582 |

|

|

|

✔ |

✔ |

|

|

| Above 400% |

Citizens and LPRs |

526,891 |

|

|

|

|

✔ |

✔ |

|

|

Ineligible Non-Citizens |

627,639 |

|

|

|

|

|

✔ |

|

| Total |

|

4,034,836 |

|

|

|

|

|

|

|

Note: All populations with a ✔ in their row could be impacted by the corresponding policy; however, some policies are mutually exclusive.

Eligible LPRs are Lawful Permanent Residents who have maintained that status for at least 5 years and would be eligible for Medicaid if their income makes them eligible. Medicaid Ineligible LPRs are Lawful Permanent Residents who have not maintained that status for at least 5 years. They do not qualify for any Medicaid program, but they may be eligible for subsidies on the ACA Individual Marketplace. Ineligible Non-Citizens are non-citizens who are ineligible for both Medicaid and Individual Marketplace Subsidies, regardless of their income level. However, they may be able to purchase unsubsidized ACA health insurance plans outside of the government-run exchange.